Debt, in

becoming perpetual, is transformed into an income that feeds capitalistic

parasitism. Regardless of the debt being the one subscribed by us, or the one

labeled as public and endorsed to us by the political class, by order of the

financial system.

Contents

1 – From

currency to debt and the role of the State

2 – How to

build debt and its meek acceptance

3 –

Capitalism does exist, it is best not to forget

4 – The

role of States in the financial system’s fattening

+++++ooo+++++

1 – From

currency to debt and the role of the State

There has been a long epoch where debts

were part of the naturally occurring exchanges between people seeking to

satisfy their needs, within the interaction context amongst members of the same

community, and where usury was not part of their way of thinking. Debts were part of the natural imbalances within the

community, and had no role as differentiating and autonomous elements of

domination of creditors over debtors; credits as assets and debts as

liabilities.

The emergence of money, materialized

into salt or shells, was later focused in precious metals – mostly gold – that,

given its inalterability, corresponded to the search for stable and acceptable

goods, being easily transportable for exchange with other goods. The very material nature of money prevented

its movement in a wider commerce scope and the safety of its possessors in the

event of robbery; it was common that kings, in their war journeys, would carry

coffers with the royal treasure and, in case of financial difficulties, would

devalue the currency by replacing part of the gold by silver or copper.

In China, before the X century, and in

Italy, in the XIII century, where there was a great density of commercial

relationships with distant parties, there was a generalization of the use of

documents that certified the deposit in a bank of a certain amount of gold, which

guarantied the withdrawal by the bearer in another bank, thus being

transmissible titles. After the end of

the period of abundant gold, brought from the gulf of Guinea by the Portuguese

and ransacked in Mexico by the Spaniards, and given the huge development of

distant trading inherent to the European colonial expansion, the conclusion was

reached that there would not be enough gold deposited in banks to correspond to

the value of the transacted goods, which would weaken depositors’ trust in

banks.

The States, in the XIX century, in order

to endow the monetary systems with the populations and businesses’ general

trust, imposed the paper money issuing monopoly – the bills in use today – by

issuing banks, without however ensuring those bills’ convertibility to gold.

So, by issuing bills without a counterpart other than the population‘s trust,

the issuing banks and the States potentially assumed a debt they could never pay; and so that no one could question the

trust in the issuing bank/State, by demanding the conversion of those bills to

gold, the States come to decree those bills’ inconvertibility to gold, thus

assuming to be debtors incapable of paying their debts, in gold or by any other

means.

The United Kingdom canceled the pound’s

convertibility to gold in 1931 because the gold was in accelerated migration to

the USA where, in 1934, all the banks were forced to deposit their gold in the

Treasure in exchange for certificates. In 1944, at Bretton Woods, all of the

currencies became referenced to the dollar, the only convertible currency, at

the price of US $35.00/ounce (1 once = 31,104 g), this reference having been

altered in 1968 by Nixon to the amount of US $42.22/ounce, in response to the

USA’s corrosive external deficits, to the Vietnam war, and to France’s purchase

of gold in exchange for dollars.

Finally, in 1971, the dollar convertibility to gold was cancelled,

leaving all world currencies without any real reference other than the

population’s trust and acceptance of bills as transaction, savings, and

speculation instruments. Even the

fiction of a relationship between gold and the dollar ended up disappearing in

1976, leaving the Federal Reserve with total liberty to print bills without any

other value than the generalized acceptance of its buying power. This means that when a central bank issues

currency, it is issuing a debt certificate that it hands over to the banking

system for placing into the society, within the scope of that mechanism:

a) the central bank creates a value from nothing, bearing

in mind that, if it is in excess within the context of the circulating

currency, that value will lead to inflation, and if it is insufficient it will

promote the rise of interest taxes, hindering business. The circulating

wealth’s value, the conjuncture, and the transaction rate within the society

have to be taken into account.

b) the central bank hands over that value to an ordinary

bank, which deposits a debt document with the assigning central bank;

c) the commercial bank will hand over the equivalent value

to several clients, within the scope of what is known as a credit multiplier,

as will be explained later.

In this way, a credits and debts cascade

is generated without it being anchored in any savings, and being totally

dependent upon the existing trust in the original monetary issue. The final receivers, private individuals and

enterprises, play an essential role in this cascade when they transform their

debts into goods and, in fact, provide a basis for the whole chain; labor is

therefore at the foundation as the only and real originator creator of value.

That artificial and artful mechanism is

present in the quantitative easing used by Draghi at the ECB; a

monetary issue that will treble the balance of the Euro Zone’s central bank,

from one (in 2014) to three billion euros in 2016, with the particularity that

commercial banks, in order to hold financial

assets for their businesses, frequently hand in, as a guaranty, public

debt bonds, thus indirectly financing the states issuing those bonds, mostly

those of the EU’s south periphery.

This ECB policy is a time bomb. Firstly

because it is not generating debts’ devaluing inflation, notably of the public

ones; secondly because issuing currency aggravates public debts which, by

nature, are financially unpayable

and unsustainable from a social point of view in countries such as

Greece and Portugal; and, finally, because the monetary mass keeps ballooning

the, so called, financial markets’

speculative bubble, which will inevitably burst, the only missing piece is

knowing when.

Let us move on to the account of a Portuguese

curiosity in the XIX century.

On November 27, 1880, the English

magazine The Economist was mentioning

the instability of the markets: “European

monetary markets are becoming tired, and not without reason, of Portugal’s

constant new loans solicitation” and, five years later, it pointed out: “In Portugal’s own interest it would be

preferable that its indebtedness facilities would be restrained now”. The

European Commission and the Eurogroup are the most recent members of this

financial lineage.

The bankruptcy, in 1890, of the Baring

Brothers (118 years later the same happened to another family business, owned

by the Lehman brothers) the City’s premier financial partner of the Portuguese

government, caused it, in order to face the situation, to transfer £1 million

in gold from the Bank of Portugal to London, considerably reducing the

Portuguese reserves. The ensuing

financial crisis was compounded by the British Ultimatum, both being

demonstrations of how much worth the Portuguese sovereignty, praised by

nationalists and patriots, has been; the republican revolt of January 31st

1891 was a well-timed exploitation of the situation. In the middle of the

crisis the “The Economist” used a very modern terminology on its February 6th,

1892, edition: “For a long time now it

has been evident that the country (Portugal) was living above its means… An

expressive reduction of the debt obligation is inevitable…”. “Holders of Portuguese debt must consent to a

decrease of their rights, by force of the circumstances”.

As it is easily seen, imperial England

was dealing with its Portuguese half-colony with the appropriate dignity; just

as it happens today with the Bruxellois oligarchy. After so many years having

passed, the inequalities amongst the several European areas remain; but the

admission of the annulment of a substantial part of the debt is not present

within the political circles because it would entail the shrinking of the

financial system’s size and deep changes in its functioning, notwithstanding

the fact of that same revocation’s inevitability and pertinence, even if it is

silenced – eppur si muove.

2 – How to build debt and its meek

acceptance

Within the Portuguese politics (and not

only) there is a marked conservatism preponderance (also) in what regards debt

in general and public debt in particular; this attitude, of falsehood,

meekness, or ignorance, sets up a curtain that hides debt’s deep meaning and is substantiated in three

ways:

a)

the failure to regard debt – public or private – as an

instrument built by capitalism for capturing peoples and lives;

that thought does not even graze the political class members’ meninges, in

particular those of the segment that boasts being the working class defender;

b)

not much visibility is given to those opinions that

challenge the debts’ legitimacy, given the prevailing pride of “not being a

deadbeat”, a pride which is in complete disharmony with the corruption

practices in place in the occidental European country which got the bronze

medal in that championship;

c)

debt is observed with resignation, in an economist[1]

way, with the political class’ opinions being divided into “we obediently pay”

and “we obediently pay but we’d

appreciate some small favor”.

3 – Capitalism

does exist, it is best not to forget

In order to overcome its accumulation

difficulties, the highly globalized capitalism, grounded on an acerbic

competition between multinational corporations, causes a fierce fight for the

planet’s resources which transforms large areas into war and environmental

devastation scenarios.

Its existence has been based on the

pressure over labor costs, and the need to invest in the production of goods

and services in order to beat the competition, as elements to increase capital

accumulation. As will be seen further ahead, the increasing financial aspect of

everything has been pushing that accumulation with the creation of

capital-money in a totally deregulated way, as in the golem[2]

tale, where the monster created to bring security is inadvertently released and

threatens the whole planet’s social structure.

Ø In the competition for selling goods and services, labor costs’

depreciation, in terms of the effective salary, as well as the prolongation of

working hours, are essential policies, in total contradiction with the productivity that technological

development has afforded. Besides that, the global production dominated by the

multinationals is segmented because of, amongst other reasons, the exploitation

of the so called competitive advantages, where low labor costs, undignified

conditions, and the meager rights imposed on the workers are included. In

summary, each degree of working skills is, intrinsically, a market within the

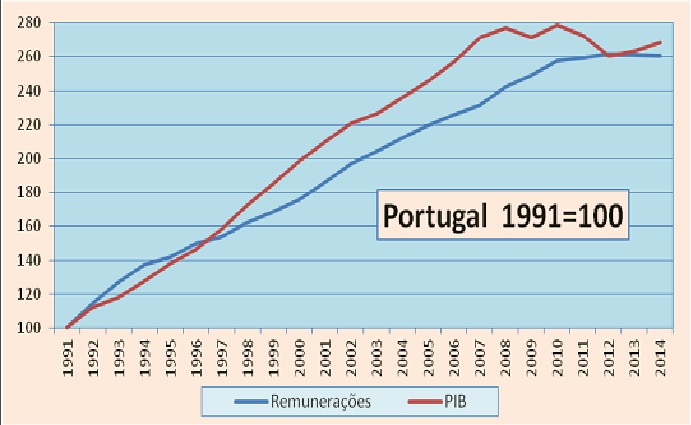

context of a globalized “labor market”. In the following graphic, the salaries’

stagnation in the USA industry showcases that tendency.

The same can be seen in Portugal where, for the last 25 years, the slow

and progressive loss of importance of the work compensation relatively to other

income, exposes the lack of claiming ability of the workers, bounded by

partisan syndicate bureaucracies.

Remunerações = Earnings PIB = GDP

Huge pouches of unemployed and

sub-employed are, thus, created, workers without papers, poor or precarious, in

addition to pensioners pressed by the ongoing hijacking of the accumulated

deductions towards the social security systems. Large segments of workers in

stupefying and underpaid bureaucratic functions are also created, as is the

general norm in a bureaucracy. They fill military and police apparatuses

without any function other than preventing threats to the power of the capital;

judicial and fiscal systems mired down in crime cases, ordinary conflicts,

collection, fines and penalties; the multinationals gigantic administrative,

marketing or sales apparatuses, replicated in small and medium enterprises;

surveillance functions in public buildings and places; data handling; etc.

This context of pressure over

labor wages, in order to guarantee low production costs for goods or services,

does not result in a sufficiency that satisfies the invested capital´s

reproduction needs, as required to keep pace with the competition, which gives

rise to the known tendency to lower the profit margins; nor is an adequate

demand for buying of those goods or services created, even if urged by an

invasive publicity.

Ø In addition to those elements dealing with salaries and other labor

related aspects, there is another essential element that blocks capitalism –

the lack of investment. On the one hand, the pressure on labor prices favors

the generation of profits, but the competition and the technological evolution

demand productivity gains, demand investment, mergers and acquisitions between

companies which, however, do not avoid the tendency to the low profit margins,

even when eliminating operators. Actually, in the great majority of the

activity sectors, the domination of a few enterprises can be seen, with the presence

of other, smaller ones, where salaries and profits are lower as are the

investment capabilities; the situations of free competition between small

enterprises are very few, as described by Adam Smith.

Before the recent neoliberalism domination, the discussion

was about the German and Japanese models (to which the soviet’s state

capitalism could be added), the integration of the big industry and the national banking capital,

with the creation of the financial capital, a designation coined by Hilferding

in 1910[3]

and later adopted by Lenin. That formulation was touted as a counterpoint to

the Anglo-Saxon management model, that separated those sectors so that the

banking capital and the financial institutions in general would be free from

the bonds of financing the industrial sectors and their management, and could

very flexibly dedicate themselves as title holders, intervening in enterprises

namely in mergers and acquisitions, which are followed by “downsizing”,

redefinition, and dimensioning actions

and that, in rule, include dismissals. Evidently, it is the Anglo-Saxon[4]

originated version which has been predominant as an ingredient of

neoliberalism.

As is natural to capitalism, capitals tend to move to

those businesses that can maximize their profitability, as compared to other

activities. From a profitability point of view, the financial system stands out

through financial, real estate, or goods (the “commodities”) speculation, from the armament industry or several

traffics such as migrants, drugs, organs, weapons… with several ad hoc fiscal benevolence formulas being created, the well-known offshore addresses, in the heart of the

most sacred of current times’ liberties – that of capital movements.

The financial “investment” being more profitable than

investing in the production of goods and services, the majority of capitalists

prefers to place their peculium on those so called financial markets with have

more flexible applications, faster profits accounting, instantaneous even,

rather than acquiring modern equipment, trying to beat the competition, risking

the emergence of technological changes, habits, fashions, etc. before the

equipment is technically or financially amortized, when it is known that the

commitment with that equipment cannot easily be brought back to a money-capital

status. This contrasts with the conversion of capital invested in the financial

roulette which is easy, instantaneously doable, decided by computer algorithms.

In the chaotic crisscrossing of several action lines,

the satisfaction or not, thereof, of natural human needs is a random variable

which keeps busy the forecast institutes[5] armed with powerful computers,

dozens of Nobel prize laureates, courts of college professors, and of whose

results we have already given a few

examples. Folks, it only matters if it has

employability, as they say in the neoliberal neo-language.

Ø With the populations’ current income scarcely satisfying their needs,

namely of those deriving their income from work, it becomes even scarcer when

one needs to find “in the market” the satisfaction of one’s elementary rights,

such as housing; and, additionally, to correspond to the consumption appeals

disseminated by the media – namely

cars, travel, fashionable household appliances. As a consequence, the financial

system generally facilitates credit and its lasting formulation, debt, as a

mechanism to capture future income, eventually for life; because, in

capitalism, people themselves are considered goods, the debt mechanism

transforms a person’s life into capitalist property.

Several elements are part and parcel of that

internalization of debt as a trivial need. One is the house buying debt, since the neoliberals handed over the

fulfillment of that elementary

need to the blessed market, to the joy of banks and the public corruption

involved in that process; and to the supreme misfortune of those that, having

become unemployed, lost their houses but kept part of their debt.

The other element is made up of debts with very high

interest rates, to satisfy consumption needs, the short term debts from credit

card use, in addition to commissions and several fees which banks are allowed

to levy, even if having a bank account with associated cards is, in fact, a

state imposition. Acceptance of the normality of having a debt is a form of

ideological capture by Capital.

As the private debt is circumscribed to one

individual, a family, a company, the risk is relatively high, even with

guarantees, because, in the case of default, it is of little value for the

financial system to seize houses and companies, since it aims not to manage

devalued real estate or recover more or less bankrupt companies. Those

guarantees mainly are a debtor’s gag because, in the case of default, they

promote the debtor’s ruin.

In Portugal, during the nineties, banks held credit

rights over many bankrupt companies’ land parcels and factories, so they

channeled them to real estate projects, transforming the losses into new

credits with high profit margins; never did they act to recover them as

industrial enterprises. They simultaneously stimulated a housing boom, which the State and the political class never

took care of, as well as the drift of public and public-private investment

towards highways and pharaonic endeavors such as Expo-98 and football stadiums.

4 – The

role of States in the financial system’s fattening

During the eighties the global financial

system, with the IMF/World Bank at its head, forced the so called Third World

countries to take on debt as a means to prey upon, privatize, and integrate

those countries into the global market, to the detriment of any of those

peoples’ well-being logic, and enlisting the local political classes to that

end, resorting to brutal dictatorships when needed (Chile, Brazil,

Argentina…) Because extreme poverty was

the rule in many of those countries and the middle class was not numerous (or was

in an accelerated process of losing purchasing power,) substantial indebtedness

by families was not viable; and the enterprises of the third-word matrix were

either public or had foreign capital.

This highlights the importance of

peoples’ capture by the State and its oligarchies, civilian or military, with

the setting up of enormous public

debts. Within this context, through fiscal punishment, the State transfers

income from the poor – without any capability to access bank credit – to the

financial system… via public debt. In the aged European societies, the

pensioners, for instance, are not a population segment with the capacity for a

(bigger) indebtedness but everyone has seen, through the fiscal load, a part of

their income captured as a contribution to pay the public debt’s obligations.

Contrarily to what is said, the

nation-states do no go bankrupt because they always have a population compelled

to finance the debt trap, as they cannot massively escape and because there is

a fiscal and judicial repression mechanism to force payment; in extreme cases

the creditors will accept losses, as in the case of Greece in 2012, or

reschedule the debts, easing the nearest instalments and burdening the midterm

payments. Thus, it is much more appealing to the financial system to accept

public debt bonds without getting directly involved in indebtedness or in

collecting from populations with difficulties, therefore using the states and

the political classes for that intermediation. In other words, the financial

systems develop mechanisms for the creation of perpetual revenues on their

behalf through the generation of public debt, and each political class fulfills

their role of distributing it by the population, the task of internally and

unevenly mutualizing the debt, of course.

In Europe, in the case of the EU or of

the Euro Zone’s dismantling, as well as of lonely exits from those

institutions, the identity based isolationism would facilitate the financial

system’s purpose of creating perpetual income in the form of debt. If it has

not been possible until now to build platforms for the erection of a solidary

union of the European peoples, each nation-state entrenched within its borders,

their flag on the castle’s keep and circulating their own

currency, would

become a much easier prey for the globalized financial capital, its boycotts

and blackmailing.

Wittingly or not, the “patriotish”

drifts held by Le Pen and its metastases spread throughout Europe, if they

prevail, will bring wide smiles to the face of the global financial capital,

and their protagonists will accept the role of peoples’ hangmen with a ferocity

that the gangs enrolled in the PPE or S&D have not used until now. It

should be recalled that the Weimar Republic, even with the assassination of

Rosa Luxemburg and Karl Liebknecht, fell far short of the III Reich’s assassin

barbarity.

4.1 – Bill

Clinton put the monster on the loose

The financial system’s drift from

productive activity towards autonomy immensely benefited from Bill Clinton’s

revocation, in 1999, of the Glass-Steagall law promulgated by Roosevelt in 1933

in order to guarantee a stable connection between savings and investment and

avoid the systemic contagion of the speculation activity. Without the

separation of commercial and investment (read: speculation) banks, money would

be able to grow in an unheard-of way, without limitations, with commercial

banks also being able to join speculation and, in this way, compromising not

only their role in financing enterprises but also the private deposits and, in

result, all of the planet’s economic activity, since truly national systems have

ceased to exist[6].

For instance, in 2013 the Deutsche

Bank’s

liabilities

regarding derivatives were worth about 16 times the German GDP, rendering this

bank too big to fail and placing it

under the loving protection of Merkel and Schauble. The global debt, public or

private, was computed by the IMF as $152 billion of which $50 billion are

states’ responsibilities – equivalent to 225% of the world’s GDP (contrast with

Footnote 5 on page 8). Hence,

the sum of public debts was equivalent to 75% of the global GDP, 133.7% in the

Portuguese case.

On the other hand, both companies and

private citizens also found in the speculative voluptuousness ways to increase

their capital and savings, benefiting from the higher margins available in the

financial area as well as of their titles’ conversion easiness to and from

money. In this way, the “normal” economy of goods and services production was

incorporated into the financial capital’s logic, seeking to obtain high yields

in order to get credit at interesting rates and, thus, maintain the constant

appreciation of their stock exchange’s quoted titles, royally paying

their upper management with “stock

options” so that they would show interest in the title’s appreciation.

Let us suppose that a bank accepts a

deposit in the value of 1000, knowing that during the deposit’s term it can use

that money minus a fraction of, say, 10% as required by the central bank. Thus, the bank can loan 900 to a client who,

for instance, will use it to make a purchase through a debit card and that

money goes to the vendor’s account. The

initial 1000 has been converted into a deposited total of 1900 and a granted

credit of 900, this exercise being repeated as many times as needed, where the

second deposit can be the base for an 810 loan, and so on. Hence the banks’

zeal to be part of the companies and people’s transactions in order to capture

a maximum volume of deposits to be multiplied as credits, knowing that only a

residual part of the global deposits’ volume returns daily to private

pockets. This mechanism is known as

credit multiplier and is the banks’ privilege; a private individual is unable

to act in the same way.

This scheme works whenever depositors

trust their bank, or the set of banks, as keepers of their money because, when

this trust fails, a rush to the banks can ensue, with the insolvent banks

keeping their doors closed and guarded by the police (Argentina) or it can lead

to a limitation on money withdrawals being imposed, as happened in Greece in

2015, where an unusual situation occurred when more money existed in peoples’

hands than in banks’ deposits. The fear of unexpected financial crises leads

States, in collusion with the financial system, to reduce as much as possible

the possession of physical money by people, and even to entertain the thought

of making all money

virtual.

After credit granting operations like

those exemplified before, a bank can pick a set of those credits and divide

their sum total into several titles which are then made available to the market

and acquired by elements of the financial system itself - securitization. The

original creditor relinquishes part of the profits it collects from the

effective debtors, in exchange for recovering the major part of the loaned capital

and being able to use it again, in this way starting a new credit chain. The

buyers of those titles will, in turn, use them together with others of

different provenances and proceed with other title conversions; this

multiplication is in the form of a Ponzi pyramid, a conman who, in the last

century’s eighties, had a replica in Portugal: D. Branca. As can be seen, this

formula increases the obligations’ volume in an unparalleled way, generates a

tangle of debts articulated as a card castle that, when it collapses, hits the

peoples through the loss of their savings, their jobs, and the imposition of

austerity plans by the political classes which, acting as proxies for the

financial system, are willing to use the public funds to lessen the latter’s

losses. In this instance, the banks’ salvation is realized through bail-ins or bail-outs,

designations that represent, respectively, the sacrifice of the share-holders

or of the general population, forced by the State to participate in the

recapitalization done by the service vector, the political class, which,

naturally, does not ask the population weather it is willing to help a bank in

difficulty.

It can also be deducted that, beyond the

first links in the chain of titles issued in the title conversion operations,

each taker knows whom they were bought from but knows nothing of the operations

included in the preceding phases; and knows even less about the identity or

solvability of the original debtor. If one of more default situations by the

original debtors does exist, the original loaning bank will support the loss,

leaving the waterfall unaffected. The problem arises in a crisis situation if

many debtors fall into bankruptcy or unemployment, ceasing payments, and if the

guarantees become devalued, preventing the bank from recovering the outstanding

debt; this is what happened with the famous subprime

in the end of 2007, which were very high risk loans granted to poor families,

enticed by financial institutions insinuating that their houses were

gaining value and that they could increase their debts by using them as

guarantee. Until one day…

Following the financial crisis of

2007/08, and despite its violence, States and the financial system did not

implement the announced measures for reducing banks’ size and debt volume, more

regulation, less complex derivative products, etc. The scare entered a shocked

state with the survival of the speculation machinery that sustains today’s

neoliberal capitalism, then went away, but contemplates with apprehension the

sky’s leaden color.

The aforementioned survival spirit,

associated with the taming of the political classes and the absence of

significant social contestation, lead instead to the growth of the banking

system and debt, with no slowdown in mergers and capital concentrations, which

surpass even the ones of before the crisis, and to 45% of the transactions

happening far away from the majestic

regulators’[7] noses

which, by that same reason, would be better named as strainers. According to

the same source, global debt ascends to 285% of the GDP and shares’ prices grow

without any correspondence with enterprises’ performance, as a consequence of

the careless issuing of financial means by the central banks, “the typical

outcome of which is a burst”.

Additionally, it is asserted that the risk to the Fed and ECB

supervisors, that hold public or private debt equivalent to 13% and 9% of the

USA and Euro Zone GDPs, respectively, is enormous. To that end, the same article considers that

exiting the very low interest rates conjuncture is necessary, but also that it

will be dramatic if this is not accompanied by a notable income growth for

families and enterprises. And that looks very difficult to happen because the

growth of interest rates, when linked to issuing smaller monetary volumes,

causes accrued difficulties to enterprises and larger state debt obligations.

(to be continued)

[1] This economics view,

which is completely tuned with the capitalist development compendiums in their

current neoliberal version, finds a liminal assertion in the resolution Project

456/XII (2nd) dated 19/2/2012, presented to the Portuguese Republic

Assembly by the Communist Party and aiming to renegotiate the public debt, from

which the following precious statements are lifted:

· “… as the Communist Party has always said, the

consolidation of the public accounts and debt reduction has to be obtained with

economic growth…” (page 2) which means that, in Portugal, people will have to

work more and more without any consideration being given to changing the relationship capital/labor, ways to redistribute income,

etc.;

· “Renegotiate debt is, after all, to guarantee its

payment, which will not be possible without the generation of wealth” (page 3);

that means, if we’re to be good boys and girls we’ll pay forever the debt we

are forced to assume, we will become your dedicated tenants. In really there is

no wealth creation that does not become a rent on behalf of the financial

system, the restructuring becoming, if it happens, a mere supermarket gift;

· The “complete and rigorous determination of the debt’s

dimension … to be carried on by the Finance Ministry and the Bank of Portugal”;

in reality, one is trusting the impartiality, the love of the people of the

PSD/CDS coalition lead by the psychopath Passos, to evaluate debt, as if it

were the sole consequence of ill devised agreements rather than the setting up

by the financial system of a capture machine of the European periphery’s

peoples. It should be recalled that the PSD leader Passos Coelho, before

winning the elections and in a trip he took across Europe to present himself,

mentioned to Angela Merkel that he would order a debt audit, an idea that the

Chancellor immediately rejected.

· The IAC – the Initiative for a Citizen Audit –

appeared towards the end of 2011, under BE’s auspices, and was launched with

pomp and circumstance with the presence of lofty foreign technicians and the

usual useless personas from the Lusitanian unitary intelligentsia. In May of

2013, the IAC declared its complete collapse by means of a proposal that would

be laughable, if it were not absolutely reactionary.

[2] The golem as

interpreted by António Negri and Michael Hardt in “Empire”

[3] We do not use this

meaning for financial capital, which we find overtaken by reality. We prefer to

consider it as a set of shares, bonds, securities, shareholder positions,

derivatives, and other instruments, transacted inside or outside of stock

exchanges, hold by an opaque and mutable set of enterprises, funds, mere

acronyms of offshore registrations, which hold goods or services producing enterprises, simple goods (the commodities) and insurance or

transportation contracts as instruments of speculation, always with a logic of

generating and accumulating capital.

[4] On this dichotomy

between capital arrangements see “Capitalism against Capitalism” by Michael

Albert (1992).

[5] Even elements of great importance to the

understanding of reality are subject to great discrepancies which reveal the

gauging deficiencies of problems’ dimensions. The “Emerging Markets” magazine

recently placed the non-financial public and private debt at $162 billion as

compared to $152 billion pointed out by the IMF. However, the magazine also

added the financial entities’ debt ($54 trillion) – that the IMF does not take

into account – which places the global debt at the $216 trillion level, about

327% of the global GDP; that means more than three years of the wealth

generated by the world population!

[6] However, every time a

bank risks collapse, the bank’s hosting country people are the ones that are

called to contribute to cover the uncollectable credits turned to losses which,

in turn, force a recapitalization or bankruptcy as was exemplarily seen in the

cases of BPN, Banif, or BES, in Portugal or, in a more extensive way, in Spain.

In other words, the profits are joyously transferred to offshores; as for the losses, those stay at home.

[7] Carlos Costa shined

in the BES and Banif cases, just as Vítor Constancio had

won, in the BPN case, enough prestige to get a vice-presidency seat at the ECB.

Sem comentários:

Enviar um comentário